Fed’s Williams says low neutral interest rates a ‘warning sign’

WASHINGTON

John Williams, president of the Federal Reserve Bank of San Francisco, speaks in San Francisco, California March 27, 2015.

Reuters/Robert Galbraith – RTR4V7IP

San Francisco Federal Reserve President John Williams said on Friday that low neutral interest rates are a warning sign of possible changes in the U.S. economy that the central bank does not fully understand.

“I see this as more of a warning, a red flag that there’s something going on here that isn’t in the models, that we maybe don’t understand as well as we think, and we should dig down deep deeper and try to figure this out better,” he said during a panel discussion at the Brookings Institute in Washington.

Williams, who is a voting member of the Fed’s policy-setting panel through the end of the year, has said the central bank should begin to raise interest rates soon but thereafter go at a gradual pace.

He added that the low neutral interest rate had “pretty significant” implications for monetary policy, and put more focus on fiscal policy as a response.

“If we could come up with better fiscal policy, find a way to have the economy grow faster or have a stronger natural rate of interest, then that takes the pressure off of us to try to come up with other ways to do it, like through a large balance sheet or having a higher inflation target,” Williams said. “It also means we don’t have to turn to quantitative easing and other policies as much.”

It has been a long time since the Bureau of Labor Statistics (BLS) published the real unemployment numbers for all Americans who fit the criteria of being able to work in the economy, but have not been able to find a job for one reason or another. Instead, the BLS has simply changed their data models numerous times since 1980, and now we have reached the point where there are actually more people between the ages of 16-54 who don’t have a job versus those in that same age range who do.

And with the Federal Reserve using these BLS numbers as the catalyst for whether to raise interest rates after nine years of them being pushed down to near zero, one regional central bank on Oct. 2 laid the blame for there being over 94 million Americans out of work and not counted in the unemployment models as simply ‘not wanting to get a job’.

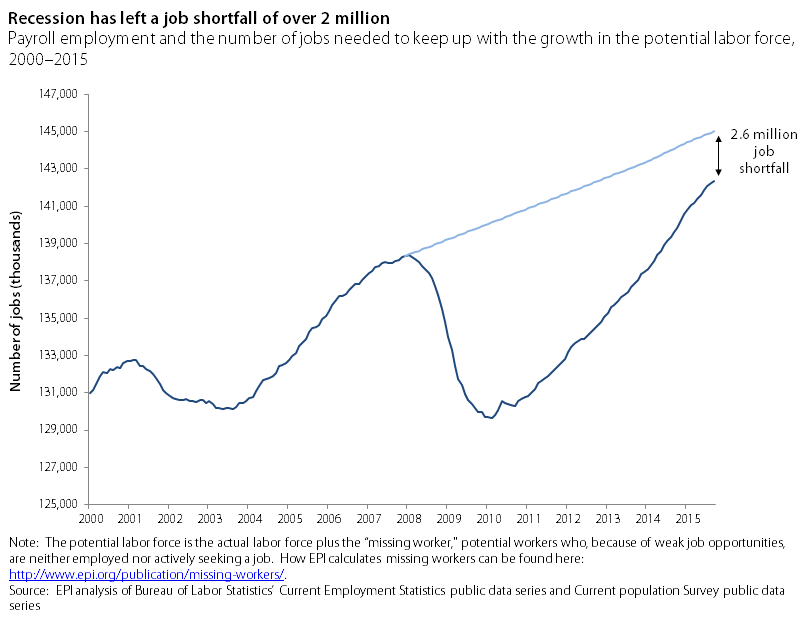

The especially poor September jobs report reinforces what many economists have been saying for months: The six-year recovery from the Great Recession has been too weak to create enough jobs for America’s growing population, let alone restore significant wage growth.

Domestic fiscal austerity, not recent global volatility, is primarily to blame for the inadequate job growth, these economists argue.

The U.S. economy created 142,000 jobs in September, bringing average monthly job growth to 198,000 this year — way down from the monthly rate of 260,000 in 2014. Average hourly wages decreased slightly in September, meaning pay has risen just 2.2 percent in the past 12 months.

In addition, the percentage of the population working or looking for work has dropped to 62.4 percent, the lowest it has been during the Obama presidency. The progressive Economic Policy Institute estimates that we need 2.6 million more jobs to keep up with population growth.

Obama, Geithner and the Missing Six Trillion Dollars

by ROB URIE

Timothy Geithner, President Barack Obama’s first Treasury Secretary and chief architect of many of the various and sundry bank bailouts and associated programs carried out during Mr. Obama’s first term in office, recently wrote a book telling his side of ‘the story.’ To be clear, I haven’t read the book and have no intention of doing so. Life is short and the relevant side of the story, the economic consequences of Mr. Geithner’s policies, is the one of interest here. The prevailing storyline in the banker’s ghettoes of New York and London is of an indispensable and functioning financial system saved and a second Great Depression averted through Mr. Geithner’s necessary but unpopular programs to transfer public resources to nominally private corporations— Wall Street banks, in order to save them. Implied is that the travails Wall Street faced in 2008 – 2009 were the result of ‘natural’ forces and that its restoration is substantially related to restoration of ‘the economy.’ Mainstream economists have put forward variations on this latter claim through repeated assertion that ‘the economy,’ as measured by GDP (Gross Domestic Product) and the official unemployment rate, has ‘recovered’ to pre-recession levels.

Graph (1): Contrary to the view on Wall Street and within the Western economic establishment restoration of Wall Street has not ‘fixed’ the economy. The policies of Mr. Geithner, the Obama administration and the Federal Reserve have ‘fixed’ profits, compensation and bonuses for Wall Street. The drop in median income is evidence of ongoing economic Depression for most citizens of the West. Assertions to the contrary by Mr. Geithner, the Obama administration and the ‘eternal sunshine of the spotless mind’ crowd of Western economists are evidence of whose interests they represent. Apparent in the recovery of financial profits without a recovery in household incomes is that Wall Street doesn’t need a functioning economy to earn ‘profits.’

Is the Fed “tapering”? Did the Fed really cut its bond purchases during the three month period November 2013 through January 2014? Apparently not if foreign holders of Treasuries are unloading them.

From November 2013 through January 2014 Belgium with a GDP of $480 billion purchased $141.2 billion of US Treasury bonds. Somehow Belgium came up with enough money to allocate during a 3-month period 29 percent of its annual GDP to the purchase of US Treasury bonds.

Certainly Belgium did not have a budget surplus of $141.2 billion. Was Belgium running a trade surplus during a 3-month period equal to 29 percent of Belgium GDP?

No, Belgium’s trade and current accounts are in deficit.

Did Belgium’s central bank print $141.2 billion worth of euros in order to make the purchase?

No, Belgium is a member of the euro system, and its central bank cannot increase the money supply.

So where did the $141.2 billion come from?

There is only one source. The money came from the US Federal Reserve, and the purchase was laundered through Belgium in order to hide the fact that actual Federal Reserve bond purchases during November 2013 through January 2014 were $112 billion per month.

In other words, during those 3 months there was a sharp rise in bond purchases by the Fed. The Fed’s actual bond purchases for those three months are $27 billion per month above the original $85 billion monthly purchase and $47 billion above the official $65 billion monthly purchase at that time. (In March 2014, official QE was tapered to $55 billion per month and to $45 billion for May.)

Why did the Federal Reserve have to purchase so many bonds above the announced amounts and why did the Fed have to launder and hide the purchase?

Some country or countries, unknown at this time, for reasons we do not know dumped $104 billion in Treasuries in one week.

Managing Director of the International Monetary Fund Christine Lagarde gestures as she delivers a closing statement to the media during a press conference at the G-20 Finance Ministers and Central Bank Governors meeting in Sydney, Australia, Sunday, Feb. 23, 2014.(AP Photo/Rob Griffith)

SYDNEY — Finance chiefs from the 20 largest economies agreed Sunday to implement policies that will boost world GDP by more than $2 trillion over the coming five years.

Australian Treasurer Joe Hockey, who hosted the Group of 20 meeting in Sydney, said the commitment from the G-20 finance ministers and central bankers was “unprecedented.”

The world economy has sputtered since the 2008 financial crisis and global recession that followed. Progress in returning economic growth to pre-crisis levels has been hampered by austerity policies in Europe, high unemployment in the U.S. and a cooling of China’s torrid expansion.

The centerpiece of the $2 trillion commitment made at the Sydney meeting is to boost the combined gross domestic product of G-20 countries by 2 percent above the levels expected for the next five years, possibly creating tens of millions of new jobs. World GDP was about $72 trillion in 2012.

The G-20 combines the world’s major industrialized and developing countries from the United States to Saudi Arabia and China, representing about 85 percent of the global economy.

The communique from the meeting said signs of improvement in the global economy are welcome but growth remains below the rates needed to get people back into work and to meet their aspirations.

Many have used a pyramid to describe the power structure that the bulk of humanity is subject to – in even the smallest details of our lives. I would like to use it here to address the impending economic collapse, with an eye to explaining what might be going on behind the curtain – what is being hidden and why.

The vertical axis of the pyramid is often described as power, wealth, knowledge, etc. The shape of the pyramid describes the population distribution as measured by the vertical axis. The great bulk of humanity (us) inhabits the lower levels near the base, and the Controllers/Powers That Be/Elites inhabit the lofty levels near the peak.

Control of events at the macro level is administered from the top down by inducing divisions through particular areas in the pyramid. These divisions are made through the use of lies that are designed to achieve particular ends such as war, population reduction, strengthened control, wealth redistribution, etc, right down to plain misery and suffering of the masses.

This pyramidal system of divisions works so well because, at the micro level, we are walking pyramids – telling lies to ourselves and others about the nature of our inner and outer realities. And in between the top and bottom there are all manner of corporations, organizations, states, and groups that take on this pyramidal structure. So pyramids fit within pyramids, while efforts to control and manipulate repeatedly divides people. As above, so below.

In general, most divisions that we can see clearly (sometimes well after the fact) are induced across the lower levels of the pyramid as history can attest (local wars, uprisings, protests, politics). The level in the pyramid at which such division originates may be low and motivated by some private interest gain. But on rare occasions a division is introduced vertically down the pyramid, affecting nearly all levels at the same time. One of these is coming in the form of the collapse of the US Dollar Reserve currency.

Would the collapse of the US dollar come as a surprise? History tells us it shouldn’t. On its current trajectory, it seems destined to go the way every other fiat currency in history has gone – towards destruction and collapse. Money creation via debt issuance must be balanced with economic growth. As the debt burden increases, growth increase is required, and when this growth falters, so does the entire system unless the debt is expunged. So, the only questions for the Dollar are:

When will collapse happen?

and;

Is there a finger hovering above the “Destruct” button?

The difference this time around is that the whole world would be affected if and when a new currency Reserve is selected as a medium for the global balance of trade.

For many, the refusal of most to even consider what seems to me to be a fairly imminent and inevitable collapse, and prepare for its consequences, is an excellent example of normalcy bias – a form of wishful thinking that paralyzes rational thought processes. If yesterday was the same as the day before, then tomorrow will be the same as today.

The US Constitution clearly states that Congress shall coin money of gold and silver. So, what happened to the US dollar? Despite the best efforts of some good folks – among them past presidents – we ended up with a privately owned Central Bank, the Federal Reserve. Federal Reserve notes (paper currency) originally declared direct convertibility to gold, but this was lost to US citizens when gold was confiscated by FDR and revalued upward to $35 per ounce from $20.67, devaluing the dollar by 40% (and attracting much foreign gold into the country). After World War II, the Bretton Woods Agreement among nations established the US dollar as a World Reserve currency and provided for convertibility to gold for any nation’s positive trade balance held in dollars. But by 1971 the US gold stock had plummeted from 25,000 tons (at peak) to 8,000 tons. Then Nixon closed the gold convertibility window, and the entire Dollar Reserve system became nothing more than a paper promise (Ponzi pyramid).

Published time: November 12, 2013 17:16

Edited time: November 12, 2013 18:14

Michael Nagle / Getty Images / AFP

A former Federal Reserve employee responsible for managing the agency’s quantitative easing program has written an op-ed apologizing for what he called “the greatest backdoor Wall Street bailout of all time.”

Writing in the Wall Street Journal, Andrew Huszar detailed his concerns about the Fed’s massive bond-buying measures. He argued that while the Reserve initially claimed the program would lower borrowing rates for average citizens, the trillion-dollar initiative primarily ended up lining the pockets of Wall Street executives.

“Despite the Fed’s rhetoric, my program wasn’t helping to make credit any more accessible for the average American,” Huszar wrote. “The banks were only issuing fewer and fewer loans. More insidiously, whatever credit they were extending wasn’t getting much cheaper. QE may have been driving down the wholesale cost for banks to make loans, but Wall Street was pocketing most of the extra cash.”

What’s more, Huszar claimed that several Federal Reserve managers expressed apprehension over the effects of quantitative easing (QE) only to find their concerns ignored.

“Our warnings fell on deaf ears,” he wrote. “In the past, Fed leaders—even if they ultimately erred—would have worried obsessively about the costs versus the benefits of any major initiative. Now the only obsession seemed to be with the newest survey of financial-market expectations or the latest in-person feedback from Wall Street’s leading bankers and hedge-fund managers.”

The mainstream media never talks about that. They are much too busy covering the latest dogfights in Washington and what Justin Bieber has been up to. And most Americans seem to think that if the Dow keeps setting new all-time highs that everything must be okay. Sadly, that is not the case at all. Right now, the U.S. economy is exhibiting all of the classic symptoms of a bubble economy. You can see this when you step back and take a longer-term view of things. Over the past decade, we have added more than 10 trillion dollars to the national debt. But most Americans have shown very little concern as the balance on our national credit card has soared from 6 trillion dollars to nearly 17 trillion dollars. Meanwhile, Wall Street has been transformed into the biggest casino on the planet, and much of the new money that the Federal Reserve has been recklessly printing up has gone into stocks. But the Dow does not keep setting new records because the underlying economic fundamentals are good. Rather, the reckless euphoria that we are seeing in the financial markets right now reminds me very much of 1929. Margin debt is absolutely soaring, and every time that happens a crash rapidly follows. But this time when a crash happens it could very well be unlike anything that we have ever seen before. The top 25 U.S. banks have more than 212 trillion dollars of exposure to derivatives combined, and when that house of cards comes crashing down there is no way that anyone will be able to prop it back up. After all, U.S. GDP for an entire year is only a bit more than 15 trillion dollars.

But most Americans are only focused on the short-term because the mainstream media is only focused on the short-term. Things are good this week and things were good last week, so there is nothing to worry about, right?

Unfortunately, economic reality is not going to change even if all of us try to ignore it. Those that are willing to take an honest look at what is coming down the road are very troubled. For example, Bill Gross of PIMCO says that his firm sees “bubbles everywhere”…

We see bubbles everywhere, and that is not to be dramatic and not to suggest they will pop immediately. I just suggested in the bond market with a bubble in treasuries and bubble in narrow credit spreads and high-yield prices, that perhaps there is a significant distortion there. Having said that, it suggests that as long as the FED and Bank of Japan and other Central Banks keep writing checks and do not withdraw, then the bubble can be supported as in blowing bubbles. They are blowing bubbles. When that stops there will be repercussions.

And unfortunately, it is not just the United States that has a bubble economy. In fact, the gigantic financial bubble over in Japan may burst before our own financial bubble does. The following is from a recent article by Graham Summers…

First and foremost, Japan is the second largest bond market in the world. If Japan’s sovereign bonds continue to fall, pushing rates higher, then there has been a tectonic shift in the global financial system. Remember the impact that Greece had on asset prices? Greece’s bond market is less than 3% of Japan’s in size.

For multiple decades, Japanese bonds have been considered “risk free.” As a result of this, investors have been willing to lend money to Japan at extremely low rates. This has allowed Japan’s economy, the second largest in the world, to putter along marginally.

So if Japanese bonds begin to implode, this means that:

1) The second largest bond market in the world is entering a bear market (along with commensurate liquidations and redemptions by institutional investors around the globe).

2) The second largest economy in the world will collapse (along with the impact on global exports).

Both of these are truly epic problems for the financial system.

If you know someone that actually believes that the U.S. economy is in good shape, just show them the statistics in this article. When you step back and look at the long-term trends, it is undeniable what is happening to us. We are in the midst of a horrifying economic decline that is the result of decades of very bad decisions. 30 years ago, the U.S. national debt was about one trillion dollars. Today, it is almost 17 trillion dollars. 40 years ago, the total amount of debt in the United States was about 2 trillion dollars. Today, it is more than 56 trillion dollars. At the same time that we have been running up all of this debt, our economic infrastructure and our ability to produce wealth has been absolutely gutted. Since 2001, the United States has lost more than 56,000 manufacturing facilities and millions of good jobs have been shipped overseas. Our share of global GDP declined from 31.8 percent in 2001 to 21.6 percent in 2011. The percentage of Americans that are self-employed is at a record low, and the percentage of Americans that are dependent on the government is at a record high. The U.S. economy is a complete and total mess, and it is time that we faced the truth.

The following are 40 statistics about the fall of the U.S. economy that are almost too crazy to believe…

#1 Back in 1980, the U.S. national debt was less than one trillion dollars. Today, it is rapidly approaching 17 trillion dollars…

#3 The U.S. national debt is now more than 23 times larger than it was when Jimmy Carter became president.

#4 If you started paying off just the new debt that the U.S. has accumulated during the Obama administration at the rate of one dollar per second, it would take more than 184,000 years to pay it off.

#5 The federal government is stealing more than 100 million dollars from our children and our grandchildren every single hour of every single day.

#6 Back in 1970, the total amount of debt in the United States (government debt + business debt + consumer debt, etc.) was less than 2 trillion dollars. Today it is over 56 trillion dollars…

#7 According to the World Bank, U.S. GDP accounted for 31.8 percent of all global economic activity in 2001. That number dropped to 21.6 percent in 2011.

#8 The United States has fallen in the global economic competitiveness rankings compiled by the World Economic Forum for four years in a row.

#9 According to The Economist, the United States was the best place in the world to be born into back in 1988. Today, the United States is only tied for 16th place.

#10 Incredibly, more than 56,000 manufacturing facilities in the United States have been permanently shut down since 2001.

#11 There are less Americans working in manufacturing today than there was in 1950 even though the population of the country has more than doubled since then.

#13 When NAFTA was pushed through Congress in 1993, the United States had a trade surplus with Mexico of 1.6 billion dollars. By 2010, we had a trade deficit with Mexico of 61.6 billion dollars.

#14 Back in 1985, our trade deficit with China was approximately 6 million dollars (million with a little “m”) for the entire year. In 2012, our trade deficit with China was 315 billion dollars. That was the largest trade deficit that one nation has had with another nation in the history of the world.

#15 Overall, the United States has run a trade deficit of more than 8 trillion dollars with the rest of the world since 1975.

#16 According to the Economic Policy Institute, the United States is losing half a million jobs to China every single year.

An increasing number of people have complained about governments and central banks in recent years, even using the word “tyranny” to describe them. They are, of course, called names in the establishment press: conspiracy theorists, mainly.

Calling someone a name, however, does not erase their argument (at least not among rational people) and both the governments and the big banks stand accused.

Up till now, however, these accusations were never accepted by the general public. The average guy really didn’t want to hear about the evils of government money. After all, that was the only thing he had ever used to buy food, clothes, gasoline, cars, and so on. He didn’t want to acknowledge the accusations because he feared what might happen to him without his usual money.

Now, however, we have a brand new currency (called Bitcoin) available to us: something radically different. This gives us a new way to directly address the subject of monetary tyranny, providing a clear test for the governments and money masters of the world:

If they are truly NOT tyrannical, they will leave this new currency alone.

In other words, Bitcoin is a test for “the powers that be.” The way they deal with this new method of exchange will reveal their true nature.

If they ignore Bitcoin, they refute the charges of tyranny. If they attack it, they verify those charges.

After all, what honest reason could there be to attack an inherently peaceful tool for transferring value?

Prospective Reasons

Reasons to attack Bitcoin have recently appeared in the “public square.” Here are the three most popular ones, each followed with some analysis:

1. It can be used for money laundering.

Of course it can be used for money laundering — ANY currency can be used for money laundering. Currencies are neutral — that is their purpose! Currencies are valuable precisely because they can be exchanged for anything else — that’s why we use them!

Moreover, dollars and Euros and Pounds are used for money laundering every day. Consider the recent money laundering crimes of HSBC and Wachovia/Wells Fargo. These banks laundered hundreds of billions of dollars for violent drug cartels. And consider that this amount of laundered money is several hundred times the value of every Bitcoin in existence.

No one from either bank went to jail. Neither bank was shut down. Neither bank suffered more than a minor fine. So, how much of a concern can money laundering really be to governments and banks? Clearly not much.

But, since they accuse Bitcoin of being used for bad things, let’s be clear about the situation:

— Every mafioso uses government money.

— Every drug smuggler uses government money.

— Every terrorist uses government money.

— Every pornographer uses government money.

— Every criminal of every type uses government money.

They also use the telephone system and the mail and banks and a wide variety of government services. But government money is good and Bitcoin is bad?

The argument fails.

2. It could destabilize the current system.

A tiny, new currency is a threat to the long-established king of the hill? Comparing Bitcoin to dollars, Euros and Yen is like comparing an ant to a dinosaur. This is a threat?

Please understand also that no one is forcing anyone to use Bitcoin. If you don’t think it’s a great idea, you don’t have to use it. If its price movements (relative to dollars) bother you, you don’t have to use it. How is that destabilizing to the current system? It is entirely separate.

And what of the current system? It was falling apart on its own before the Bitcoin program was ever written. And I could go on at length on the insane levels of government debt, hundreds of trillions in derivatives, rehypothecation, and innocent people being forced to bail-out failed banks.

The current system has massive problems, but none of them can be blamed on Bitcoin.

This argument fails also.

3. Bitcoin provides no customer protection.

Well, no, it doesn’t. Bitcoin is a currency, not a legal system.

What is implied by this argument is that the government banking system does protect customers. That is an outright lie. People are ripped-off via the banking system every day. And more than that, consider what happened just a month ago in Cyprus: Thousands of innocent people were ripped-off BY the banking system — purposely — all at once and without recourse. This argument is, really, an insult to one’s intelligence.

And I should add something else: If Bitcoin is used properly, the crime of identity theft (a big problem with government money) vanishes — there is no identity available to be stolen.

So, again, the argument fails. Only those people who believe anything a government says will buy it.

In the End

In the end, it is said, we judge ourselves. Bitcoin has now put governments and banks in the position of judging themselves. They will write their own verdicts.

It should be interesting to watch.

[Editor’s Note: Paul Rosenberg is the “outside the Matrix” author of FreemansPerspective.com, a collection of insights on topics ranging from Internet privacy and economic freedom, to alternative currencies. Join our free e-letter list to receive other articles like this one… and immediately get a report that explains in a unique way how the US Government got into the mess it’s in, the dangers that creates for us, and how to protect ourselves from it.]

Germany and The Central Bank are Pressuring Cyprus to steal from it’s citizens as and answer for fiscal irresponsibility. The Central Bank has ordered banks to block citizens access to their own personal accounts. Thereby barring access to their own money. I suppose they are biding their time making sure that people do not empty their accounts before the decision to allow them to steal the money is reached.

Since when is this kind of blatant theft not an unlawful act? Who do they EU and the Central Bank think they are to be coercing the government to commit this crime against it’s people?

Cyprus’s central bank has written to the island’s lenders to ask them to block customer’s transfers and payments, according to reports on the island.

Cypriot website 24h revealed on Sunday that the Central Bank of Cyprus wrote to Cypriot lenders on Saturday, March 16 to ask them to stop all form of payments from their accounts, even those that were from one account at the bank to another.

The measure comes after the Eurogroup asked Cyprus to impose a one-off tax on depositors as part of its bailout.

Kathimerini English Edition understands that the capital controls do not apply to the units of Cypriot banks in Greece. Normal restrictions on cash withdrawals and electronic transfers are in place.

The depositor tax will not apply to Cypriot bank units in Greece but the branches are set to be absored by a Greek lender by Tuesday.

The proposed levy had caused an outcry among many Cypriots

Germany’s finance minister has warned Cyprus that its crisis-stricken banks may never be able to reopen if it rejects the terms of a bailout.

Wolfgang Schaeuble said major Cypriot banks were “insolvent if there are no emergency funds”.

He was speaking after the Cypriot parliament rejected an international bailout deal that would have imposed a one-off tax on bank deposits.

Frantic talks are under way to try to agree an alternative plan.

Leaders of political parties in Cyprus are due to meet later after parliament rejected the controversial levy, proposed as part of a 10bn-euro (£8.7bn; $13bn) bailout package.

The BBC’s Mark Lowen, in Nicosia, says the country is in turmoil and the eurozone’s plan has completely unravelled,

Analysis

Mark Lowen BBC News, Nicosia

There may have been jubilation among many Cypriots at Tuesday night’s parliamentary defeat of the hated banking tax, but now the country faces a tough reality.

The EU bailout has been derailed and Cyprus is edging towards bankruptcy. But talks are also continuing with the EU to find a credible alternative.

The eurozone’s third smallest economy has just sent a resounding message of defiance to Brussels. And the impact will spread far beyond this tiny island.

Not a single MP voted in favour of the controversial deal, sending a clear message to Brussels that the strategy needs a drastic rethink, our correspondent adds.

Late on Tuesday, Mr Schaeuble said that he “regretted” the vote.

“The ECB (European Central Bank) has made it clear that without a reform programme for Cyprus the aid can’t continue. Someone has to explain this to the Cypriots and I think there’s a danger that they won’t be able to open the banks again at all,” he said.

“Two big Cypriot banks are insolvent if there are no emergency funds from the European Central Bank,” Mr Schaeuble added.

Cypriot President Nicos Anastasiades called the talks between party leaders when it became clear that the measure would not be passed by parliament.

Fearing a run on accounts, Cyprus has shut its banks until at least Thursday. The local stock exchange also remains closed.

Cyprus’ banks were badly exposed to Greece, which has itself been the recipient of two huge bailouts.

People line up at an ATM in Nicosia to withdraw cash on Thursday.

Patrick Baz/AFP/Getty Images

The clock is ticking on Cyprus’ fiscal cliff.

The European Central Bank has given the Mediterranean country just four days to come up with its own bailout plan, or a eurozone lifeline to its struggling banks will be severed.

The ultimatum comes after Cypriot lawmakers on Tuesday rejected a highly unpopular proposal put forward by the European Central bank, the European Commission and the International Monetary Fund to give the country’s banks half of a $13 billion bailout package if they can raise the other half from a steep levy on the country’s personal savings accounts.

Since then, the Cyprus government has been struggling to come up with a “Plan B” that will satisfy international lenders. If Cyprus can’t do it by Monday, the ECB will pull the plug on Cypriot banks, which would likely precipitate a collapse of the island’s financial institutions and send shock waves through European and world markets.

Update at 2:40 p.m. ET: Cyprus Bank To Be Restructured:

NPR’s Joanna Kakissis reports that the governor of Cyprus’ central bank, Panicos Demetriades, says country’s second largest bank, Cyprus Popular Bank, will be restructured to forestall its imminent collapse next week. Cyprus Popular Bank has placed a $336 (260 euro) limit on ATM withdrawals.

Our original post:

Kakissis, reporting from the Cypriot capital Nicosia, says the country’s banks were drained by exposure to the Greek debt crisis. But EU and IMF leaders see the island as a haven for offshore investment, especially by wealthy Russians, and want depositors to pay for part of a bailout.

Banks have been closed until Tuesday to prevent a bank run, but ATMs have been restocked so people can withdraw money, Kakissis says.

The Parliament in Cyprus could vote on a plan to raise the $7.5 billion as early as Thursday

Of course people will protest. They have closed the banks and block access to their money. I would dare say it is a very logical reaction to being robbed,wouldn’t you ?

And yet it is typical of this type of strong arm tactic for the victim to be treated as the criminal,while the criminal is protected. Truly ironic is it not ?

Demonstrators outside the House of Representatives yesterday wearing Angela Merkel masks

AROUND 1,000 people gathered outside Parliament yesterday despite a vote on the proposed haircut being postponed until today at 6pm.

Around half of the protesters dispersed quite quickly after receiving news that the vote had been put back, planning on regrouping outside the House today.

“I’m here for the same reason as everyone else to protest the bill and we will come tomorrow and the next day if required,” 56-year-old insurance salesman Lambros Kannaouros said.

“The decision to make the people pay is unfair,” he added.

Petros Heracleous a 26-year-old unemployed protester believed that attempts to restructure the haircut were pre-planned to make the people think that the politicians were trying to change something. “We prefer to keep our pride instead of suffering the repercussions of a haircut,” he said.

Forty-year-old telecommunications regulator, Yiannos Demetriou felt that a haircut would go against human rights and against the Cyprus constitution. “They are trying to take advantage of us so they can take our natural gas and impose a solution to the Cyprus problem that will suit foreign powers,” he said. “If Anastasiades is assuming the political cost of the haircut then he should call for a referendum or even call a general election,” he added.

Cyprus finance minister Michalis Saris arrives to meet his Russian counterpart in Moscow. Photo:

Banks in Cyprus are to remain closed on Thursday and Friday, the government has said, amid continuing uncertainty over an EU bailout that required a 10 per cent tax on savings.

President Nicos Anastasiades will chair a meeting with the parliamentary party leaders tomorrow at 9.30am at the Presidential Palace.

Russian Prime Minister Dmitry Medvedev has criticised the EU and Cyprus’ handling of the country’s ongoing economic crisis, saying they are acting “like a bull in a china shop”, the state-run news agency RIA Novosti reported.

Meanwhile, Prime Minister David Cameron has reaffirmed that any British military or government personnel in Cyprus would not lose their savings due to the crisis.

Local news in Cyprus is reporting an escalation in the protests that have begun in the wake of attempts by EU chiefs to confiscate the savings of depositors. The news of possible bank closures has enraged the public. It appears that in order to keep things under control, the Central Bank is discussing a possible bank merger rather than a full shut down.

The Central Bank of Cyprus today intervened to quash frantic reports that Cyprus Popular Bank is to be closed down.

The reports sent hundreds of Cyprus Popular Bank employees and holders of the bank’s bonds out into the streets. Police deployed a strong force outside the Bank’s headquarters in the capital Nicosia to prevent them smashing into the building. (Source)

Here is a video showing police in riot gear on the scene:

Cyprus Broadcasting Corporation says the following:

The European Central Bank today said it had decided to allow the Central Bank of Cyprus to keep providing banks with emergency funding until this coming Monday.

An ECB statement said that thereafter, Emergency Liquidity Assistance can only be considered if a rescue programme is in place that would ensure the solvency of the banks involved. (Source)

Meanwhile, President Anastasiades supposedly has a Plan B ready:

Cyprus’s political leadership today decided on a package of measures dubbed “plan B” to avert a financial meltdown, as the finance minister is engaged in rescue talks with Russian officials in Moscow….

No details of the plan were immediately announced, but Averof Neophytou, a close associate of President Nicos Anastasiades said that there had been a unanimous decision to establish a “Solidarity Fund”. (Source)

Recent photos of the protests were posted at ZeroHedge, which you can see HERE. One protester can be seen holding a sign that says, “Where is the solidarity?”

We’ll keep you posted as this develops. Previous updates and videos can be found below…

ATMs in Cyprus were drained over the weekend, electronic transfers were halted, and riots ensued following a decision by European Union chiefs to raid private savings accounts to help pay for the country’s $13 billion bailout. It was believed that there were plans to stretch a bank holiday to at least one week, while the exact measures were decided upon. However, yesterday the Cypriot parliament rejected the scheme outright, leading many to speculate that this would be the start of something even worse.

Sure enough, much like the U.S. Federal Reserve threatened martial law and blood in the streets if Congress didn’t accept sweeping bailouts in 2008, now Germany is saying that Cypriot banks might never reopen after parliament’s decision:

Germany’s finance minister, Wolfgang Schaeuble said major Cypriot banks were “insolvent if there are no emergency funds,” according to a BBC report, meaning savers might lose all their money if no deal was reached. (Source)

There is extreme worry that if the banks do reopen, capital flight is all but assured. Meanwhile, similar confiscation schemes are being proposed for Italy and New Zealand (more on that below), spurring questions about which other nations are in line for a “haircut” . . . perhaps better called “the chopping block.”

Whether or not Cyprus gets its bailout in one form or another — perhaps from Russia — this is a precedent-setting crisis that is already leading to such a level of distrust in Cyprus that merchants are even refusing credit card payments. This is indeed shaping up to be a potential “Lehman Brothers Moment” with ramifications that could extend even beyond the troubled nations of Europe.

The euro zone agreed on Saturday to hand Cyprus a bailout worth 10 billion euros ($13 billion), but demanded depositors in its banks forfeit some money to stave off bankruptcy despite the risk of a wider run on savings.

….

In a radical departure from previous aid packages – and one that gave rise to incredulity and anger across the country – euro zone finance ministers forced Cyprus’ savers to pay up to 10 percent of their deposits to raise almost 6 billion euros.

Cyprus president Nicos Anastasiades agreed to the deal, which completely reversed his previous assurances that it would not happen. It sets a very dangerous precedent for future bailouts. As if brutal austerity wasn’t enough, the EU is now demanding a bailout tax making citizens and expat depositors alike personally liable for government and private bank debts. Reuters also notes that according to a draft of the legislation, criminal penalties of up to 3 years in jail and 50,000 euros could be imposed upon anyone who doesn’t comply.

Most of the 10 billion euros will go to bail out Cypriot banks, which took a blow when their substantial holdings of Greek government bonds were written down as part of that country’s second bailout.

Britain has 60,000 depositors in Cypriot banks, including thousands of military and government personnel stationed on the island. George Osborne highlighted that Cypriot banks in England would not be subjected to the tax (originally proposed at 6.75% for accounts under 100,000 Euros; 9.9% for those over 100,000), but expat depositors apparently will — government and military excluded:

George Osborne vowed today that those serving in Britain’s military or government in Cyprus will be protected after European finance chiefs ordered an unprecedented raid on personal bank accounts.

Up to 60,000 British savers are to lose thousands of pounds each as expats in Cyprus have their savings decimated in part of a painful bid to bail out the bankrupt island.

The Chancellor said the financial situation in Cyprus was ‘an example of what happens if you don’t show the world that you can pay your way’, adding: ‘We are not part of the bailout.’ (Source)

The tax is being justified as a last-ditch effort to raise money and keep Cyprus from supposedly causing a domino effect across the Eurozone as indebted nations begin to collapse. Cyprus had set itself up as a strong banking center for investors, but many are outraged over Anastasiades’ about-face:

Those affected will include rich Russians with deposits in Cyprus and Europeans who have retired to the island, as well as Cypriots themselves.

“I’m furious,” said Chris Drake, a former Middle East correspondent for the BBC who lives in Cyprus. “There were plenty of opportunities to take our money out; we didn’t because we were promised it was a red line which would not be crossed.”

“I’ve lost several thousand,” he told Reuters.

ZeroHedge reports that it is those “rich Russians” who could wind up angriest. Eurogroup had suggested that depositors under 100,000 euros should maintain their insurance against such a scheme, but it is possible that larger depositors will absorb their percentage by moving the top percentage tax to 15.6%.

The Eurogroup will give Cyprus more flexibility on bank levy, and that Cyprus should safeguard depositors under €100,000, even as the full €5.8 billion deposit goal must still be hit.

….

(The) Russian response to the discovery that haircuts on big deposits just rose from 9.9% to over 15.6% will hardly be warm and cuddly. Now may be a good time to ban gun (and plutonium) sales to angry Russian billionaire oligarchs. (Source)

However, the changes continue today, 3/19.

The President just proposed the ‘levy’ on deposits begin at EUR 20,000 just hours ahead of today’s planned vote.

CYPRUS REVISED BILL SEES NO LEVY ON DEPOSITS UP TO EU 20,000

However, it is still theft of private property which appears to be the philosophical stumbling block for the parties involved and therefore today’s vote appears to be delayed:

ANASTASIADES TO MEET PARTY LEADERS 9 AM TOMORROW: SPOKESPERSON

CYPRUS PARLIAMENT BANK-LEVY VOTE MAY HAPPEN TOMORROW, CYBC SAYS (Source)

Members of the troika of international lenders arrive at the Presidential Palace yesterday (Christos Theodorides)

THE government yesterday ordered banks to stay shut until next week as it toyed with the idea of re-submitting a proposal on tax deposits – at a much lower rate than the previous scheme – as it scrambled to avert a financial meltdown.

The government was yesterday trying to find alternative solutions after parliament on Tuesday rejected the terms of a bailout from the European Union and turned instead to Russia for a lifeline.

“We don’t have days or weeks, we have only hours to save our country,” Averof Neophytou, ruling DISY deputy chairman, told reporters as crisis talks in Nicosia dragged into the evening.

Neophytou tried to get the message through to other parties.

“I believe we will not be the cursed generation of politicians who will let our country go bankrupt,” Neophytou added.

It was suggested yesterday that the government may submit a bill today proposing a haircut on deposits but at lower rates than legislation that was rejected by parliament on Tuesday.

MPs threw out a proposed tax on bank deposits in exchange for a €10-billion bailout from the EU, a stunning rejection of the kind of strict austerity accepted over the past three years by crisis-hit Greece, Portugal, Ireland, Spain and Italy.

The tax — 6.7 per cent on deposits under €100,000 and 9.9 per cent on deposits over €100,000 — was designed to fetch the government €5.8 billion.

The shortfall from the lower rates could be covered by nationalising the provident funds of semi-state companies.

Bank of Cyprus vice president Evdokimos Xenophontos said the situation could be reversed but warned against touching foreign deposits.

“We cannot do it to foreign depositors who trusted us. This could be theft,” he told reporters after meeting President Nicos Anastasiades last night.

Xenophontos said only Cypriots must foot the bill in exchange for bank warrants, better interest rates, etc.

“If we protect them (foreigners) even if they leave, they will come back. We lived through an invasion and we overcame the difficulties on our own,” he said.

THE NUMBER of non-Cypriots living on the island number over 170.000, the vast majority of whom would have Cypriot bank accounts and are would be affected by a deposit haircut.

The full figure of 170,383 is from the population census carried out by the statistical services in October 2011, published in January this year.

Of the 170,383 non-Cypriots living in Cyprus at the time, 106,270 were EU citizens and 64,113 were non-European. From the European citizens, statistics show that the number of Greeks was the highest at 29,321, then Britons at 24,046, Romanians 23,706, and Bulgarians 18,536.

From the non-European citizen, Filippinos numbered 9,413, Russians 8,164, Sri Lankans 7,269, and Vietnamese 7,028.

Greeks, Romanians and Bulgarians mainly resided in Nicosia while most UK citizens resided in coastal areas such as, Paphos during the research period. The majority of Russian citizens resided in Limassol.

From the non-European citizens the majority lived in Nicosia.

“The population census is carried out once every ten years,” Georgia Ioannou, a statistics officer said. “Since 1982, we have been conducting this survey on October 1. We do not do the survey during the summer period as many people are on holiday and we also do not want to visit people’s homes during Christmas or Easter,” she said.

“We use the traditional method of going from home to home with a questionnaire. We mark down all residents of Cyprus who have been in the country for more than one year or are planning to stay for over a year,” Ioannou said.

The population of Cyprus during the latest population census was 840,407 people, 431,627 were women compared to 408,780 men. From the 106.270 European citizens, 53,607 were men and 52,663 were women. From the 64,113 Non-European citizens, the women were 41,114 and men were 22,999.

ATMs in Cyprus were drained over the weekend, electronic transfers were halted, and riots ensued following a decision by European Union chiefs to raid private savings accounts to help pay for the country’s $13 billion bailout. It was believed that there were plans to stretch a bank holiday to at least one week, while the exact measures were decided upon. However, yesterday the Cypriot parliament rejected the scheme outright, leading many to speculate that this would be the start of something even worse.

Sure enough, much like the U.S. Federal Reserve threatened martial law and blood in the streets if Congress didn’t accept sweeping bailouts in 2008, now Germany is saying that Cypriot banks might never reopen after parliament’s decision:

Germany’s finance minister, Wolfgang Schaeuble said major Cypriot banks were “insolvent if there are no emergency funds,” according to a BBC report, meaning savers might lose all their money if no deal was reached. (Source) There is extreme worry that if the banks do reopen, capital flight is all but assured. Meanwhile, similar confiscation schemes are being proposed for Italy and New Zealand (more on that below), spurring questions about which other nations are in line for a “haircut” . . . perhaps better called “the chopping block.”

Whether or not Cyprus gets its bailout in one form or another — perhaps from Russia — this is a precedent-setting crisis that is already leading to such a level of distrust in Cyprus that merchants are even refusing credit card payments. This is indeed shaping up to be a potential “Lehman Brothers Moment” with ramifications that could extend even beyond the troubled nations of Europe.

The euro zone agreed on Saturday to hand Cyprus a bailout worth 10 billion euros ($13 billion), but demanded depositors in its banks forfeit some money to stave off bankruptcy despite the risk of a wider run on savings.

….

In a radical departure from previous aid packages – and one that gave rise to incredulity and anger across the country – euro zone finance ministers forced Cyprus’ savers to pay up to 10 percent of their deposits to raise almost 6 billion euros.

Cyprus president Nicos Anastasiades agreed to the deal, which completely reversed his previous assurances that it would not happen. It sets a very dangerous precedent for future bailouts. As if brutal austerity wasn’t enough, the EU is now demanding a bailout tax making citizens and expat depositors alike personally liable for government and private bank debts. Reuters also notes that according to a draft of the legislation, criminal penalties of up to 3 years in jail and 50,000 euros could be imposed upon anyone who doesn’t comply.

The Cypriot central bank has denied reports today that stricken Cyprus Popular Bank, the island’s second-largest lender, is to be closed down, Reuters is reporting.

“We deny these reports. Efforts are under way right now to find the best possible solution for this bank,” Central Bank spokeswoman Aliki Stylianou told state television.

A man reads a note on the shutters of a Cyprus Popular Bank (CPB) branch informing customers that the bank will remain closed. Credit: Reuters

Cyprus pins hopes on creation of solidarity fund as ECB threatens to cut off lending

Political leaders in Cyprus have agreed that their country should form an investment fund to raise the capital needed to agree a bailout with the eurozone and International Monetary Fund and avert a collapse of its banking system.

The deputy leader of Cyprus’s conservative DISY party Averof Neofytou announced the agreement within a few hours of the European Central Bank saying that it was set to cut off lending to insolvent Cypriot banks on Monday.

“We will find a solution,” said Neofytou. “We have no other choice. We are making a united effort to avoid our country’s bankruptcy and I think we will succeed.”

Nicosia plans to create a fund collateralized by state assets, possibly including natural gas revenues, church property and social security fund reserves. A proposal is due to be submitted to the House of Representatives on Thursday evening.

A government official who declined to be named told Bloomberg that some kind of deposit tax was not being ruled out.

Meanwhile, Finance Minister Michalis Sarris continued talks in Moscow, with Cyprus hoping there would be Russian interest in Cypriot banks or in contributing to the investment fund being created.

Sarris told Cypriot state broadcaster that he would meet two Russian ministers on Thursday evening and that the main aim would be to convince Moscow to invest in the wealth fund to be set up by the Nicosia government.

“We are asking for help clearly, but something that would make also economic sense for Russia,” Sarris told reporters earlier.

Cyprus is also asking Moscow to extend the maturity of an existing 2.5-billion-euro loan. Sarris said that Russia was unable to provide Cyprus with a new loan.

Neofytou said that Cyprus would welcome Russian assistance but still needed to balance this against the requirements of remaining in the eurozone.

“We cannot reject any form of help but we are in the euros and we need the continue support of the ECB for liquidity,” he said. “Any support is welcome but we should not forget that we are in Europe and we need European institutions to stabilize our economy.”

I seem to recall a country that was also being pressured to accept the terms of a bailout. Its people were upset and angered over the aspect of having to bailout a bank for their fiscal irresponsibility. The government listened to it’s People and rejected the terms of the bailout. Lo and behold the world did not implode and they are still there. Doing quite nicely I might add….

When I first heard Iceland was allowing its taxpayers to vote on whether or not they should repay $5.7 billion that one of its defunct banks owes the U.K. and Netherlands, the angry taxpayer in me took hold and I hoped that they’d vote against repaying.

Turns out the Icelanders felt the same the resentment and said so today when they voted down a deal to repay the British and Dutch. Their rejection essentially revolts against the idea that taxpayers should be held responsible for banks’ financial problems.

Think about it this way, if given the choice back in 2008, would you have paid your share to save AIG, or any other financial institution, and in turn its creditors?

The situation in Iceland is a little trickier than that since the institution in question was a bank, Landsbanki Islands, whose depositors included folks from Britain and the Netherlands. When Landsbanki Islands blew up in 2008 leaving depositors without their money, the British and Dutch government stepped in and bailed out their respective depositors to keep them from panicking.

Now though, those governments want that money back. And since whatever assets are left of Landsbanki Islands are not enough to recover the total $5.7 billion, the people of Iceland are left footing what remains of the bill–estimated to be around $2 billion.

Help comes from Finland, Norway, Denmark and Sweden

The IMF will pump about $827 million into the Icelandic economy immediately

The goal is to stabilize the country’s finances and shore up its currency

Iceland is facing severe recession after a series of bank failures in October

(CNN) — Nordic countries agreed to lend struggling Iceland $2.5 billion to help it recover from a series of crippling bank failures, bolstering a $2.1 billion aid package from the International Monetary Fund, their governments announced Thursday.

Prime Minister Geir Haarde has been trying to drum up support for Iceland’s bailout.

“This is a first step to get Iceland out of its current serious financial and economic situation,” the governments of Finland, Norway, Denmark and Sweden announced in a joint statement. “The banking crisis in Iceland is of unprecedented proportions and has serious implications for the country’s economy.”

The statement follows the IMF’s decision on Wednesday to pump about $827 million into the Icelandic economy immediately, with another $1.3 billion coming in eight installments. Both moves are aimed at stabilizing Iceland’s finances and shoring up its currency, which plummeted after a series of bank failures in October.

Iceland sought IMF help after its government was forced to nationalize three banks to head off a complete collapse of its financial system. Trading on the country’s stock market was suspended for nearly a week, economic growth nearly flatlined and inflation jumped to more than 12 percent.

“As a result,Iceland is facing a severe recession, given the high debt level in the economy and significant dependence of the private sector on foreign currency and inflation-indexed debt,” John Lipsky, the IMF’s acting chairman, said in a statement announcing the decision.

A look at what Putin gains—newfound economic might

It’s mere coincidence, of course. But to Vladimir Putin, the man who called the Soviet Union’s demise the “greatest geopolitical catastrophe” of the 20th century, just the thought of saving Iceland’s hide must seem like redemption.

In 1986 Iceland hosted the Reykjavik summit between Ronald Reagan and Mikhail Gorbachev, a meeting momentous for its unplanned evolution into a conversation on nuclear disarmament between the two leaders—but also as a catalyst for the 1991 August coup against Gorbachev that sparked the USSR’s implosion.

“It was a sign of change in the Soviet Union, in many ways in the decline of the Soviet Union,” says Shamil Yenikeyeff, a Russia expert at the Oxford Institute for Energy Studies.

ARC DE TRIOMPHE

Now Reykjavik is asking Moscow for a $5.5 billion emergency loan to prop up its economy after its banking system collapsed two weeks ago amid the global credit disaster. And Russia is positioned, as a revitalized once-superpower flush with cash, to rescue Iceland, a NATO member praised for its chart-topping living standard! To Putin and the Kremlin, could there be a sweeter arc to the last two decades of Russian history?

That may be putting it a bit too strongly: even if Moscow grants the loan, Iceland will need a lot more cash, probably from the International Monetary Fund’s pocket. Still, Putin’s famous lament suggests a partial answer to the question that’s abounded since reports of the loan surfaced: What’s Russia after here?

True, $5.5 billion isn’t a staggering sum for a country with around 100 times as much in cash reserves. Nor is the loan a done deal: agreement wasn’t reached in the first round of negotiations last week. But the gesture alone—even the possibility—is significant. After all, Russia was a financial and political basket case just 10 years ago and has its own economic woes at the moment.

Pride, surely, isn’t the only prize: the seas of the “High North” are rich in fish and energy resources, and Moscow needs to show the world it’s a good global citizen after trouncing Georgia this summer. But for a leadership keenly aware of Russia’s less than auspicious place in modern history texts, this is an opportunity to further demonstrate that indeed there is a new world order, and it’s not the one George H.W. Bush foresaw in 1990.

The Hunger Site – Your click helps to feed the hungry

Wheatgrass Kits.com

FAIR USE NOTICE

The material on this site is provided for educational and informational purposes. It may contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. It is being made available in an effort to advance the understanding of scientific, environmental, economic, social justice and human rights issues etc. It is believed that this constitutes a 'fair use' of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have an interest in using the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond 'fair use', you must obtain permission from the copyright owner. The information on this site does not constitute legal or technical advice.

Any materials (ie. graphics, articles , commentary) that are original to this blog are copyrighted and signed by it's creator. Said original material may be shared with attribution. Please respect the work that goes into these items and give the creator his/her credit. Just as we share articles , graphics and photos always giving credit to their creators when available. Credit and a link back to the original source is required.

If you have an issue with anything posted here or would prefer we not use it . Please contact me. Any items that are requested to be removed by the copyright owner will be removed immediately. No threats needed or lawsuit required. If there is a problem and you do not wish your work to be showcased then we will happily find an alternative from the many sources readily available from creators who would find it amenable to having their work presented to the subscribers of this feed.

Thank you for your time and attention, blessings to all :)

Economic Policy Inst

Economic Policy Inst

Video

Video  Video

Video  Video

Video  Video

Video

{kind=link}

{kind=link}

{kind=link}